Insufficient Capital June Update

Company in Focus: Earlypay (EPY:ASX)

Our first newsletter was sent on 8 May 2019 to 31 close friends and family. This quarter’s newsletter was sent to nearly 2000 people. Thank you for your continued support. Since 1 July 2019, our portfolio has outperformed the ASX200 (including dividends) by 4.9 times, with performance of 84.9% compared to ASX200 performance of 17.4% over the two financial years.

Performance Figures

The portfolio fell -3.07% over the fourth quarter of the Australian financial year, underperforming the ASX200 performance of +8.23% by -11.30%. Whilst disappointing, this quarter takes our 2021 financial year performance to a very pleasing +48.00%, outperforming the benchmark ASX200 by a significant +20.47%. The top contributor during the quarter was Healthia (HLA:ASX). The largest detractor during the quarter was EML Payments (EML:ASX). EML Payments was one of our largest positions until the Central Bank of Ireland raised “significant regulatory concerns” about anti-money laundering compliance in Prepaid Financial Services, which EML acquired last year. On 19 May, when the issues were revealed, the stock fell 49%. EML has since recouped some of these losses but is a tender reminder that a high conviction portfolio carries high volatility due to stock specific risk. We have not made any changes to our EML position and await the Central Bank of Ireland’s decision, noting that past precedents point to a financial impact less material than the valuation decrease indicates.

The portfolio currently has 3.1% cash. The largest three holdings represent 44% of the portfolio. By our own categorisations, the portfolio is split between approximately 44% ‘value’ (cash flows weighted towards the near term) and 56% ‘growth’ (cash flows weighted further into the future).

Quarterly Portfolio Changes

There were 4 small portfolio changes during the quarter, including further purchases of Earlypay (EPY:ASX), RPM Automotive (RPM:ASX) and BetMakers (BET:ASX), as well as a partial sale of Cadence Capital (CDM:ASX). All companies have been covered in prior newsletters available on our website.

Earlypay

Earlypay is a $110 million invoice financing and equipment funding business, which is highly cash generative and well-capitalised, fresh from raising $18.8 million. Earlypay was originally named CML Group and only rebranded in 2018 to the far catchier and ‘techy-sounding’ name we know today. Perhaps management hoped that the market would confuse this boring lending business for a sexy buy now pay later… although Earlypay is far too profitable and its default rate (<0.1%) far too low to make that mistake.

What is Invoice and Equipment Financing?

Invoice financing businesses front customers’ money based on their outstanding invoices. When the invoice is collected, it is paid into a separate account from which Earlypay’s fees are deducted and the proceeds are distributed to the invoicer. This type of financing is extremely popular as no security external to the invoice is required. Consequently, the financing can scale as businesses (and invoices) scale, and typically have higher approval ratings given the security of invoice. For businesses dealing in larger invoices with longer payment terms, Earlypay unlocks valuable cash flow. In FY2020, invoice financing represented 72.7% of Earlypay’s revenue and 66.5% of EBITDA. Equipment financing makes up the remaining 27.3% of Earlypay’s revenue and is relatively self-explanatory. Demand for equipment finance is supported by boisterous Australian infrastructure spending. For example, over 700 trucks and commercial vehicles are currently funded by Earlypay.

Industry Fragmentation

Both the invoice financing and equipment financing arms are heavily fragmented – we see this as an opportunity rather than a risk. Whilst the largest four Australian banks all have trade financing arms, these typically service larger businesses – Westpac for instance, start at $500,000). The integration of Skippr (addressed below) allows Earlypay to provide financing from $20,000. One recent development in the space is the re-entry of CBA into invoice financing, powered by Waddle (similar technology to Skippr, acquired by Xero late 2020). This is a fairly significant development, not only given CBA’s scale – but also given its focus beyond the typical larger businesses to SMEs starting at $50,000. The product, dubbed “Stream Working Capital”, will be a direct competitor to Earlypay’s offering. The pie is large enough for Earlypay to generate significant transaction volume with miniscule market share.

Aussie Aussie Aussie

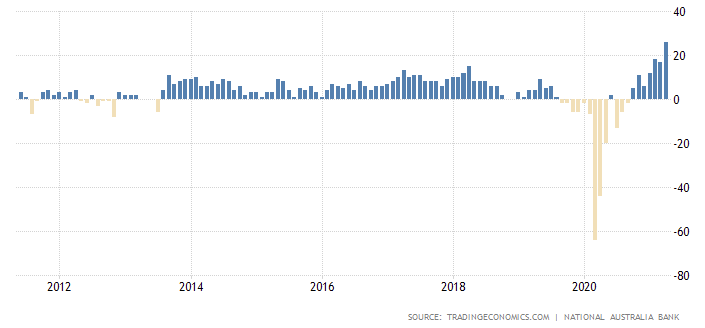

Australian business confidence is a useful barometer for SME lending appetite. With Australia fortunately coming out of the initial COVID-19 downturn far sooner than other developed nations, business confidence has returned to record highs with a vengeance amid record capacity utilisation and forward orders.

10 years of Australian business confidence (Trading Economics)

Attractive Yield and Earnings Profile

The chart below shows Earlypay’s annual dividend history since listing in 2010 and each year’s respective yields (nominal dividend in cents per share is shown in blue, approximate yield is shown in green). The average yield since listing is 5.9% and the company has paid a dividend every year since listing. Whilst we are not dividend-hungry, as stated in our ‘Ground Rules’ (see Number 9), we always look to re-invest dividends when a company offers discounted shares. Earlypay offers a lucrative 5% discount on reinvested dividends, which we will gladly participate in to cheaply fund further growth of the loan book. The 2021 expected dividend of 2.3c is sourced from management’s own forecast. Our 2022 dividend estimate of 3.2c is based on our 2022 forecast earnings per share of 5.33c and management’s target of a 60% payout ratio. This EPS equates to $11.6 million of earnings (36% growth on management’s 2021 earnings guidance) and consequently, a price to earnings ratio of circa 9X. In March, the company experienced record transaction volume of $199 million, up 34% on March 2020.

We believe that Earlypay’s acquisition of Skippr increases the quality of the firm’s earnings profile and should contribute to a higher valuation multiple of at least 12X earnings – this implies 33% 12 month upside to the current valuation.

Digital Transformation

Earlypay’s management has successfully digitally transformed the company from an old world financing business to a new world tech-enabled lender. The acquisition of Skippr’s technology platform has enabled the company to accelerate its onboarding capability of smaller sized clients from two weeks to 24 hours, and has allowed the company to service smaller businesses. Founded in 2016, Skippr is a proprietary online platform, providing invoice financing solutions to SME clients. Skippr has thus far been very successful, with over 90% of all new invoice financing clients onboarded and managed using the platform (up from 56% in the December quarter). As quoted in the Skippr acquisition presentation, an implied cost per acquired invoice financing client of $2,000 compares very favourably to Earlypay’s historical cost of acquisition of circa $20,000. Such efficiency gains will translate to an improvement in the bottom line and support our forecast increase in earnings.

Whilst Earlypay is far from the first tech enabled invoice financier, and faces challenges from Xero entering as an upstream provider, we believe that multiple smaller players can coexist. The addressable market size is vast and has sustained multiple participants for years. However, looking forward, we see Waddle (owned by Xero) as unlikely to continue supporting alternative accounting packages alongside Xero’s package (which captures ~50% of the market). With many ‘old school’ financers still operating in this space, we are confident in Earlypay’s ability to stay relevant.

A Post-Covid Tailwind

With government stimulus of the labour market having ended in March, many SMEs will require additional capital and Earlypay’s invoice financing arm will benefit from the re-adjustment to pre-Covid conditions. The equipment finance arm of the business should benefit from near-term government infrastructure projects and asset write-offs.

Knight in Invoice Financing Armour?

Earlypay has previously received acquisition offers from Scottish Pacific and Consolidated Operations Group (ASX:COG). COG offered scrip and cash valued at 48¢ a share. Scottish Pacific offered 60¢ (57¢ per share in cash and a 3¢ fully franked dividend). Whilst both deals fell through, COG retains a 17.4% ownership of Earlypay and may emerge as a suitor again.

Quip of the Quarter

“It is one of the common pieces of Wall Street experience that when the public goes stock mad and the market leaders are filled with the arrogance of prolonged success, such little things as high money rates or decreases in earnings or unraised dividends have no instant effect on the market — that is, on the state of mind of the speculating public. In the end, of course, all violations of the fundamental laws of economic and financial common sense are paid for.” – Edwin Lefevre (American journalist, writer and diplomat, best known for his novel, ‘Reminiscences of a Stock Operator’, which was inspired by legendary investor, Jesse Livermore)

This statement was first published 98 years ago.

It was appropriate back then, many times before then, many times up until today… and will be appropriate for many times to come.

The cycle of greed and fear is the only certainty in investing and is core to human nature.

We would preface this quote by noting that we do not believe the market as a whole is dramatically overvalued… COVID-19 vaccines are being successfully (for the most part) rolled out, monetary and fiscal stimulus efforts continue to be nothing short of extraordinary. That being said, it is not our job to decide whether the market is overvalued. Our only focus is on finding great businesses which can compound shareholders’ equity at a high rate.

However, it is clear that there are pockets of extreme euphoria in equity markets.

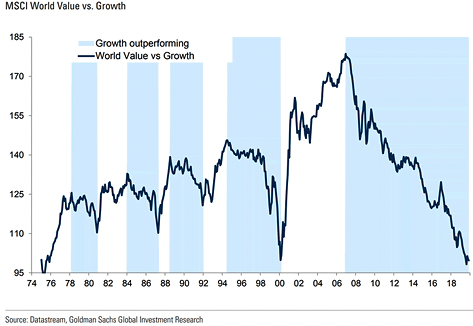

Up until very recently, ‘value’ stocks were significantly underperforming ‘growth’ stocks. Obviously, this alone does not indicate euphoria. There are currently 4323 companies listed on the NASDAQ. Of those, 794 (18%) have a market capitalisation greater than 10X their trailing 1 year revenue (Finviz) – This statistic is simply outrageous.

The underperformance of value stocks compared to growth stocks

The rise of retail investors, some of whom are relying more on ‘hot tips’ and a plethora of online forums, adds fuel to the 10X revenue fire.

SPACs, NFTs, Gamestop, Robinhood, Diamond Hands, Laser Eyes – such vernacular (and we could include much more) has only wandered into mainstream financial commentary relatively recently. Whilst we are all for progress and innovation, we worry that many people are not doing sufficient due diligence. Money is cheap… and sports betting is only legal in around half of US states.

If you would like further details regarding our activities, we encourage you to follow us on Instagram and Twitter, where we share more regular bite-sized commentary. Email us at insufficientcapital@gmail.com.