Insufficient Capital March Update

Performance Figures

The portfolio rose +16.46% over the third quarter of the Australian financial year, outperforming the ASX200 performance of +4.20% by +12.26%. This takes our financial year to date performance to +52.69%. The top contributor during the quarter was Smartpay (SMP:ASX). The largest detractor during the quarter was Afterpay (APT:ASX). The portfolio currently has 10 positions, 1.85% cash and is most heavily weighted to our ‘Structural Tailwinds’ strategy. Our structural tailwinds investments are typically classified as ‘growth’ investments, an area which is particularly topical at the moment – there is a widespread focus on the ‘reflation trade’ and ‘value rotation away from growth’ (an increased interest in traditional value investments with strong near-term cash flows). The recent increases in the risk free rate continue to threaten lofty tech valuations. Our largest three holdings represent circa 50% of total FUM (including cash).

Quarterly Portfolio Changes

There were three small portfolio additions during the quarter, including the purchase of Healthia (HLA:ASX), a burgeoning allied healthcare operator. HLA is targeting the deployment of at least $20 million of capital for the acquisition of allied healthcare businesses throughout FY2021 – this should result in continued EPS accretion, with the group benefitting from some economies of scale. More detail to come in a future newsletter.

We are still building our positions in two other portfolio additions and will disclose them in a future newsletter. Both positions are microcaps valued <$100M at time of purchase.

One addition is a tech-enabled cashflow finance provider which could pay a yield of around 6.5% over FY21. The firm is a rare beneficiary of the March wind-down in government stimulus, with increased demand for working capital across SMEs.

The other addition is a vertically integrated group of Australian automotive aftermarket businesses. The firm is making strategic acquisitions whilst organically growing their core brands and is currently valued at circa 7.5X forward EV/EBITDA, with a net cash position and close to 70% insider (members of the Board, management & vendors of previously acquired businesses) ownership.

BetMakers (ASX:BET)

In our last newsletter, we flagged that we would discuss BetMakers, a recent addition to the portfolio.

Rocky Beginnings

Investors could be forgiven for looking at BetMakers and throwing it in the ‘too hard basket’. In early 2019, the firm transitioned from a highly competitive industry to an attractive investment proposition. Founded in 2011, the company initially aimed to build B2B software products for betting companies, while also competing against them with their own retail betting business. When you are competing against large corporate bookmakers (e.g. Flutter [LON:FLTR]), the capital requirements to win and retain customers are vast. Between its listing (under the name, TopBetta) in December 2015 and June 2018, the company had not produced a dollar of positive operating cash flow. Existing investors were diluted as the company continuously tapped investors for more capital.

The Pivot

Then it all changed. The firm sold their bookmaking businesses (TopBetta and Mad Bookies) to PlayUp for $6 million and acquired Dynamic Odds (DO) and Global Betting Systems (GBS) to round out their suite of leading B2B products. BetMakers now compiles over 100 data feeds from racing jurisdictions around the world and supplies it to bookies via a single integration. They are essentially a middleman between racing authorities and bookmakers getting paid by both sides.

BetMakers produce and distribute data for racing bodies. That data is required by bookies to deliver a racing product – race fields, speed maps, commentary, official prices and live vision. The bodies charge bookmakers 2-3% of turnover to bet on their ‘product’ and pay BetMakers in return for packaging it up and also supplying the data needed to monitor the integrity of their sport. For bookies, it’s better to use BetMakers rather than linking up with every single racing body globally, and far cheaper than building in-house capabilities.

The Opportunity

BetMakers distribute over 200,000 races every year, half of which are international races into the Australian market. Clients include the majority of major corporate Australian bookies, close to 40% of the tier one bookmakers in the United Kingdom and new customers in the burgeoning United States market. These recurring, contracted revenues are being deployed into improving their products and developing new B2B revenue streams.

The company is inserting itself between more racing bodies and wagering operators, providing content and clipping the ticket on turnover. If this market grows as expected, further deals in the United States could provide significant revenue upside. To give some context, the US has 87 thoroughbred race tracks and twice as many races each year as Australia.

Sportech Acquisition

In late November 2020, BetMakers announced a transformative acquisition of three of Sportech’s core divisions. On Christmas Eve, after a competing bid for Sportech’s entire business was dismissed, Sportech shareholders voted in favour of the proposed acquisition by BET for AU$56.2 million. BET gained Sportech’s:

- Tote business (USA, Latin America, UK and Europe) – provides B2B hardware, software, support, race day controls, parimutuel pool interfacing and co-mingling to racetracks, casinos and other venues

- Americas digital business – provides white label B2B digital betting solutions to Advanced Deposit Wagering / Online Racing Bookmaker operators

- Tote software engine, “Quantum”

Post-acquisition, BET will have contracts with >95 new tote customers, >200 racetracks and venues, and >25 service agreements for white label digital betting platform solutions. The three divisions listed above generated AU$46.9 million in revenue and AU$6.9 million in EBITDA in FY20. Thus, BET is paying 1.2X EV/Sales and 8.1X EV/EBITDA for the divisions – we view this as a great deal when considering Sportech’s high quality recurring revenue and cross-sell opportunities.

Coupled with BetMakers existing business, the combined business would have delivered AU$56.1 million in revenue and AU$7.7 million in EBITDA during FY20. Furthermore, management expects strong growth from the combined business, including significant synergy and cross-sell opportunities from BetMaker’s existing operations. We believe that the business could generate over AU$10 million of EBITDA in FY22 (and ultimately, generate a 15% net margin over the long run). This would value the business at around 70X 2022 EV/EBITDA and 13X 2022 EV/Sales. We envision possible growth of 30%/annum over the next 5 years across both the top line and EBITDA line – such an achievement would render today’s valuation cheap.

By no means could we ever argue that paying today’s BetMakers multiple for any business is inherently cheap. However, we cannot reiterate enough that BetMakers’ clients simply could not function without their services. They have a symbiotic relationship. It is comparable to operating an e-commerce business through Shopify. Once a business is using Shopify, so many headaches and operational problems are alleviated that it is a pleasure to remain a loyal, loving customer… and pay Shopify an annuity stream. Shopify is currently valued at around 210X 2021 EV/EBITDA and 32X 2021 EV/Sales. In saying that, relative valuations are a very dangerous tool – when the tide is rising, ‘fair’ comparable multiples can delude even the most rational investor. We believe that such a phenomenon has occurred in the Buy Now Pay Later industry.

Describing the acquisition of Sportech as ‘transformative’ is an understatement. The acquisition massively derisks an investment in BetMakers – we expect an improved liquidity profile and increased broker coverage. At a share price of AU$1/share, BET’s market capitalisation (after raising AU$50 million at AU$0.60/share to fund the acquisition) of AU$776 million is a far cry from its prior microcap status. Pre-acquisition, the business generated <AU$1 million in EBITDA last financial year. Management can now leverage off Sportech’s existing clientele and profitability to scale the business, particularly in the United States.

A Promising Trip(p) Ahead?

In February 2021, BetMakers announced a $75 million strategic placement at $0.70/share to accelerate their global B2B wagering strategy. The placement left BetMakers with a significant net cash position of circa $110 million to continue the execution of strategic opportunities. The placement was spearheaded by industry leader, Matt Tripp, who invested $25 million. Tripp has had an illustrious career in online wagering including roles as:

Chairman of Sportsbet (March 2011 – April 2013, with numerous roles prior to 2011)

CEO of CrownBet (March 2014 – May 2020)

CEO of BetEasy (August 2018 – May 2020)

Executive Chairman of the Melbourne Storm rugby league club (May 2020 – Present)

Further to his participation in the placement, Tripp has been contracted as a strategic advisor to BetMakers, focusing on the execution of ‘strategic’ and ‘transformative’ deals.

A ‘strategic’ deal constitutes a binding transaction which stems from Tripp’s introduction or reasonable assistance and results in an increase in company revenue by more than 10% on a pro forma basis. If a ‘strategic’ deal is achieved by February 2023, Tripp will receive 35 million unquoted performance rights convertible into 35 million shares for nil consideration.

A ‘transformational’ deal constitutes a binding transaction which stems from Tripp’s introduction or reasonable assistance and results in an increase in company revenues and EBITDA by more than 100% on a pro forma basis. If a ‘transformational’ deal is achieved by February 2023, Tripp will receive 32 million unquoted performance rights convertible into 32 million shares for nil consideration as well as 32 million unquoted options at $0.70 per option.

Thus, if all rights and options are converted, Tripp will have 134,714,286 shares in BetMakers (inclusive of the $25 million original placement). This would equate to approximately 14% of the company. The deal reinforces our conviction in BetMakers’ technology, growth strategy and driven management.

Fenix Resources (ASX:FEX)

We have a small position in Fenix Resources, one of many fortunate beneficiaries of a truly meteoric rise in the iron ore price.

Fenix operates the Iron Ridge Hematite Project in the Midwest of WA. The Iron Ridge project aims to provide around 1.25mtpa of high-grade DSO for a small mine life of around 6.5 years. At first glance, Fenix and its boutique project appear atypical from our common portfolio selections. Moreover, in terms of resource investment, the project is far from compelling with respect to production scalability and potential resource growth. That being said, Fenix’s simplicity is part of its allure – its simple project metrics and economics create a compelling investment in the current commodity cycle and the company’s current position has an asymmetric risk profile.

N.B. Subsequent to the release of this presentation, the company has reached steady state production and begun shipping ore.

Fenix is currently valued at a market capitalisation of about $107m (at 23.5c/share) and is debt-free with ~$10m cash on the balance sheet – although we expect a considerable portion of this to be used in the January quarter (since about half of Iron Ridge’s capital costs are payable after commercial production is achieved). Incidentally, this will coincide with the first payments for their Iron Ore, so we are confident in the company’s ability to operate without further dilution.

Iron Ridge would not be considered a favourable operation by most investors:

- Iron Ridge is a basic project, single pit operation, with a single excavator and low-level processing. The mine is only targeting 1.25Mt of ore a year (by means of comparison, Hancock’s Roy Hill project produces >60Mtpa).

- Iron Ridge has a relatively high cost of production (estimated at $76.86/dmt FOB per Fenix’s feasibility study completed in late 2019).

- Iron Ridge’s life of mine is only 6.5 years

- Iron Ridge’s location and small scale mean that the only feasible method of transporting ore to port is trucking it 490km to Geraldton.

So what attracts us to Fenix? We view Fenix as an attractively priced call option on Iron Ore with an opportunity at present to generate enough cashflow to minimise iron ore commodity risk in subsequent years. Over the past 9 months, the company has significantly derisked itself, from obtaining its mining licence to making its first shipment of ore in late February. Furthermore, over this period, key factors affecting the underlying economics of Iron Ridge have materially improved.

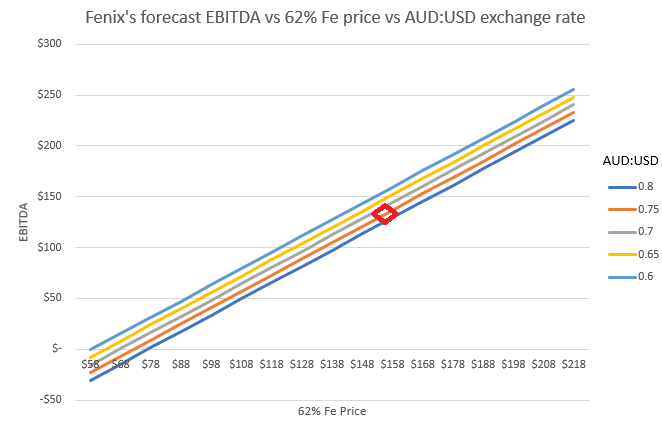

At the time of the feasibility study, Fenix reported that at an $US78/dmt price for 62% Fe and exchange rate of $US0.70/AUD, the company would achieve an average annual EBITDA of over $16.4m across the life of mine. Since then, whilst the Australian dollar has appreciated to USD$0.76/AUD, the 62% Fe index has risen over 50% in Australian dollar terms.

Fenix’s internal modelling suggests that a US$1 increase in the 62% Fe index will contribute $1.6m to EBITDA, and a US$0.01 movement in the exchange rate impacts $1.5m. Some crude back of the envelope calculations evaluate the annual EBITDA at current price and exchange rate to be somewhere north of $100m EBITDA (we get ~$130m ceteris paribus).

However, as discussed previously, the project is fairly limited and is fairly sensitive to the underlying iron ore price. The company’s $76.86/dmt FOB production cost (effectively even higher CFR cost) puts it in the higher reaches of the iron ore cost curve, and even the premium commanded by the grade is not sufficient to stop Fenix from being a relatively low margin producer.

The project’s current life is 6.5 years, and whilst further development may be able to be done, it is unclear what the economics of any development would be. In February this year, Fenix signed a farm-in agreement with neighbouring Scorpion Metals to expand Iron Ridge’s scope. Whilst we applaud management’s proactivity in looking to extend the project, the reality is that there are still significant uncertainties with this avenue. As a result, when evaluating the project, we do so at face value, ignoring any development upside.

All this considered, the elephant in the room is where the iron ore price will go – this is something we cannot predict well – indeed when we invest in the resources industry we tend to buy attractive projects with a strong margin of safety on the commodity. It would be incomplete to not address it in part. The surge in iron ore prices over the last year have come from strong Chinese demand off the back of government stimulus, as well as crippled Brazilian supply. Despite Brazil being one of only a few nations to still be posting record day on day COVID-19 infections, it appears that Vale is managing to get production and exports back on track. Recent developments in China have also created concern in the market – with steel production ordered to be cut in certain cities due to environmental concern. While we keep an eye on the global iron ore market developments, the reality is we feel that Fenix’s attractive valuation more than compensates this risk at present. Furthermore, growing Chinese environmental concern could be positive for Fenix’s higher-grade ore, which requires less coking coal to be turned into steel. We do not subscribe to any speculation surrounding a supply glut from Indonesian or African supply coming online – the larger-scale projects in these countries are still a number of years out, again Fenix’s short-term focus negates this risk.

Whilst Fenix, in our view, is unlikely to be the next Fortescue, the stars have aligned for a project delivering high cash flows, delivering what we perceive to be asymmetric risk. Management has proven themselves to be competent in project execution (starting production on schedule and even achieving steady-state production a month earlier than planned). This all works in Fenix’s favour, leading the investment thesis to boil down to a race between Fenix producing and shipping iron ore at these price levels, and Brazilian iron ore supply ramping up.

In the interests of attention span (provided that you are still reading), we will be delaying our regular ‘Quip of the Quarter’ until our next newsletter. We believe that it is a particularly significant quip which should not be tucked away at the end of a long newsletter.

If you would like further details regarding our activities, we encourage you to follow us on Instagram and Twitter, where we share more regular bite-sized commentary. Email us at insufficientcapital@gmail.com.