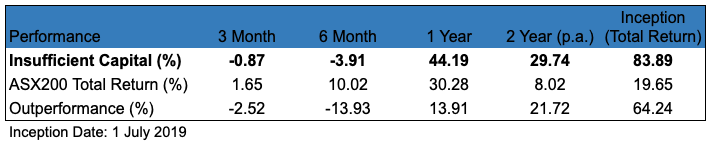

Insufficient Capital September Update

Company in Focus: Allegiance Coal (AHQ:ASX)

We would like to apologise for the late newsletter. On a personal note, all of our team have now achieved the milestone of completing undergraduate engineering degrees. How this will correlate to improved stock picking remains to be seen. The top contributor during the quarter was EML Payments (EML:ASX) and the largest drag on performance was Smartpay (SMP:ASX).

Quarterly Portfolio Changes

There were 4 small portfolio changes during the quarter, including the purchase of Allegiance Coal (AHQ:ASX) and Charter Hall Long WALE REIT (CLW:ASX). This is the first time we’ve bought a REIT for 5 years. We have a positive view on CLW’s portfolio and a mildly contrarian view that offices and physical retail stores still have a future.

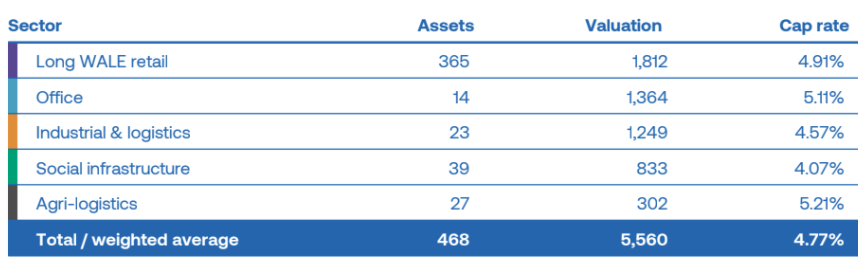

We bought the REIT at an FY2022 yield of 6.2% and a discount to net assets greater than 5%. Higher inflation will have a positive impact on the income portion of our forecast return, with 40% of leases linked to CPI and 60% with a favourable 3.1% average annual rent review. CLW is reasonably geared at 31.4%, with an extraordinarily low average cost of debt of 2.1%. A summary of CLW’s portfolio (which has a long 13.2 year weighted average lease expiry) is shown below.

Summary of CLW’s Portfolio. Source: Charter Hall Long WALE public filings

CLW has an enviable tenant mix (see below), diversified between government (20%) and non-government (80%) tenants, as well as across multiple industries. 99% of CLW’s tenants are government, ASX-listed, multinational or national businesses.

CLW’s Tenant Mix by Revenue. Source: Charter Hall Long WALE public filings.

We are particularly excited by CLW’s ‘Industrial & Logistics’ segment, which represents 22.5% of the total portfolio. Our research has led us to comparable properties selling privately on cap rates as low as 3.5%, which is 23% lower than CLW’s average ‘Industrial & Logistics’ cap rate.

REITs like CLW will rarely be large portfolio positions because they do not meet our performance target of 25%/annum. Our investment in CLW demonstrates some of the main challenges of the current environment:

- Valuations have increased significantly throughout developed equities markets, especially for US growth equities. The Nasdaq has doubled over the last two years and the average PE ratio has expanded from 24.3x to 37.7x. This decreases the number of attractive opportunities and makes our hurdle a difficult yardstick.

- Interest rates remain close to 0% despite US ‘real’ inflation running at circa 10%. There is obviously much debate about the exact figure. That 10% figure is sourced from Shadow Stats, reflecting their estimate of today’s inflation if it were calculated the same way it was in 1990. Holding cash is an incredibly unattractive proposition.

If contractionary monetary policy is finally used to dampen high real inflation, the cap rates of REITs will follow, negatively impacting real estate valuations. We hope that the quality of CLW’s portfolio and tenant mix, as well as increased distributions, will outweigh the negative impact of higher cap rates. In saying that, contractionary monetary policy could stop Australia’s multi-decade real estate party, which would be incredibly unpopular! The roaring 20s are likely to continue…

Allegiance Coal

We have been following Allegiance Coal (AHQ:ASX) for a number of months, and even more closely given the recent surge in coal prices. Allegiance is a metallurgical coal developer and operator, which owns 4 projects across North America spanning pre-approval to producing assets:

- New Elk – Ramping up Production

- Tenas (90% ownership) – Environmental Authority to be submitted end of year

- Black Warrior – Ramping up Production

- Short Creek – Pending Permitting

As opposed to thermal coal, which attracts substantial negative public sentiment given greener energy alternatives, using metallurgical (coking) coal in a blast furnace is by far the cheapest and most effective way to manufacture steel. The company trades at 60c/share, with a market capitalisation of around $210m.

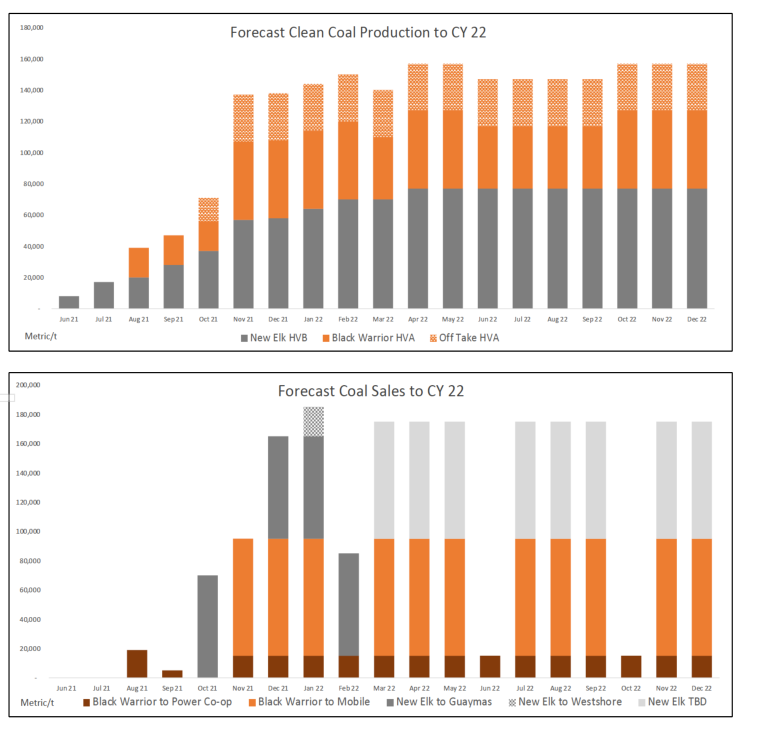

Up until mid 2020, Allegiance was a single project play, holding 90% of the Tenas project in British Columbia, Canada. In late 2020, the company acquired New Elk (a mine placed in care and maintenance by its previous owner), and began investigating ways to establish production in a capital efficient manner, noting at the time that seaborne coal prices were at a low. New Elk kicked off production in May this year and recently shipped its first cargo. Management is targeting 1.8Mtpa of High Vol B coal (ramping up to 2.5Mtpa by 2024) across a lifespan of 25+ years for the project.

In 2021, the company made two strategic acquisitions: Black Warrior mine in Alabama and Short Creek mine in Alabama. Both acquisitions were at incredibly attractive prices despite strong coal markets and have very short payback periods.

New Elk and Black Warrior are both in a ramp up phase, selling trial cargoes to Asian customers, and samples to potential buyers worldwide for testing, with the aim to switch to index-linked long term supply contracts.

Allegiance Sales and Production Profile – Insufficient Capital estimates that the company is approximately 2-4 weeks behind this schedule. Source: Allegiance Coal public filings.

Our thesis for Allegiance shares similarities with Fenix Resources (FEX:ASX), which we covered in our March newsletter:

- At the time of coverage, both had near term production (in the case of Allegiance, already producing), which will result in strong near term cash flows

- Both mined attractive products commanding a significant premium on seaborne markets

In contrast with Fenix, where we raised a few areas for concern (primarily around high production cost, single asset base introducing large project risk, short mine life – with minimal exploration potential, supply-side shocks from various other projects racing to market and a small concern over Chinese geopolitical risk with Australia), Allegiance owns a number of projects, with attractive production lives of 15+ years. Projects are on the lower end of the cost curve, with significantly less commodity price risk than Fenix (New Elk produces a blended product at about US$88/tonne; Tenas’ project economics are in the bottom quartile of costs). Allegiance is geographically diversified, not only across the US and Canada, but also with West/East Coast North American port access, allowing for flexibility to meet demand.

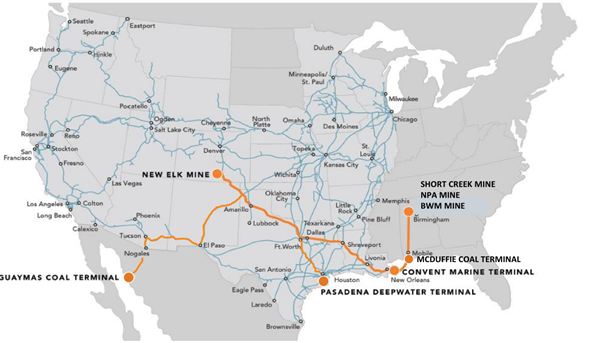

In addition to Allegiance’s ability to command a price premium from operating out of North America and having excellent access to multiple ports, the company also has significant optionality in blending coal to meet market requirements. Black Warrior, New Elk, and further offtake coal can be blended to take advantage of market demand, essentially able to extract value beyond the products by themselves.

Allegiance’s network of operating assets offer attractive blending opportunities and multiple Pacific and Atlantic port options. Source: Allegiance Coal public filings.

Beyond strategic blending opportunities and market access, management has made several accretive operationally focussed manoeuvres:

- Acquired Black Warrior in July 2021 – a previously a family run business selling high grade met coal to a local power co-op as thermal coal, realising significantly less revenue than could be commanded on the seaborne market. The mine was materially undercapitalised, and management saw an opportunity to significantly increase production at a largely similar cost of production.

- Agreed on US$25m in funding to construct a rail spur to shave US$6/tonne of unit costs for New Elk (at a production run rate of 2.5Mtpa over 25 years, the US$15m/annum of savings are significant).

- Adjusted the New Elk startup plan to approximately half upfront capital costs (given the current challenges with obtaining labour – see ‘Key Risks’, we hate to think what the full blown startup with twice as many production units from the start would have looked like).

On a macro level, ESG mandates mean that coal project financing and development (even for higher quality met projects) are not attractive to many players, reducing the risk of a supply glut even at inflated prices.

We do not believe that structural change in demand for metallurgical coal within the steel industry is relevant for a number of years, and it will take time for demand to fall. The reality is that there has never been greater demand for coal than there is today.

Key Risks

The obvious question is whether coal prices are sustainable, and although we’d like to believe they are, as a rule of thumb we don’t speculate on commodity prices.

We have also seen the company experience operational delays in scaling New Elk’s production. These are not geological, but rather with regards to acquiring a suitable labour force near Trinidad, Colorado. As such, we do not see this being a long-term issue, but certainly one that affects scaleup (N.B. Black Warrior does not appear to be facing these constraints given the strong coal mining industry in and around Birmingham, Alabama).

Furthermore, unfortunate timing with regards to securing untested trial cargoes has meant that the first seaborne cargoes from New Elk and Black Warrior have been sold at substantial discounts (on top of weaker market prices). Due to this, there are a few months of these lower margin cargoes before Allegiance is exporting at high coal prices.

That said, Allegiance is well insulated from any downturn given its low-cost operations, and low financial leverage. Somewhat to our disappointment, the recent two acquisitions have been entirely equity funded (got to keep the brokers happy!) and this has left Allegiance with a healthy balance sheet heading into a period of strong cash flow. We anticipate that management will utilise these cash flows to fund a large portion of Short Creek and Tenas, such that future dilution should be limited as the company ramps production across its portfolio.

Conclusion

Allegiance is well on track to be a mid-low cost met coal producer, shipping 5Mtpa of high grade, geographically diversified, coal in a few years. Despite some delays in startup and delayed exposure to index-linked markets, operations are scaling up and we believe that the market has assigned too great a discount for these brief inconveniences.

Given our forecast for the company to exceed $100m/annum EBITDA run rate (valuing the business at less than 2.1x EBITDA) within months at current coal price levels, the company’s multi-decade asset life with a strong development pipeline, and low costs of production, we believe that Allegiance is an incredibly compelling investment proposition with multiple traits that set it apart from other ASX coking coal companies. Furthermore, listed peers are valued at higher forward earnings multiples – Warrior Met Coal (3x EBITDA), Coronado (2.4x EBITDA), Alpha Metallurgical Resources (2.6x EBITDA), Arch Resources (2.9x EBITDA).

Quip of the Quarter

“Buy land, they’re not making it anymore.” – Mark Twain (novelist best known for his adventure stories of American boyhood).

One would expect land values to increase at a faster rate than inflation – specifically, they should follow a combination of population growth, economic growth and technological advances. Peter Lindert’s 1988 paper “Long-run Trends in American Farmland Values” discusses the consistent growth of US land values since 1805 – see Lindert’s findings below. We have split the data into two analysis periods (the first being the entire period from 1805-1980; the second being 1930-1980). From 1805-1980, CPI averaged 1.12%pa whilst land appreciated 2.02%pa (+0.9%pa real return). From 1930-1980, CPI averaged 3.24%pa whilst land appreciated 5.93%pa (+2.69%pa real return). Of course, this brings us back to the question of ‘real’ inflation. Since 1980, the Bureau of Labor Statistics altered the methodology behind CPI calculation in order to account for the substitution of products and quality improvements (e.g. newer generations of technology priced higher but more powerful – such as iPhone 8 vs iPhone 7). The 1805-1980 data range is unaffected by these changes to the CPI calculation.

However, the concept of scarcity is being turned on its head. Old-world scarce assets (such as land, gold, baseball cards, unique number plates, Ferrari 250 GTOs) are turning digital through digital certificates of authenticity, verified through a public blockchain. There are now entire decentralised digital worlds built by the community. Decentraland (which is the oldest of these worlds) has its own limited supply of ‘LAND’, which is an NFT that represents land in Decentraland. These land parcels can then be developed and economic value can be extracted by offering experiences (such as games) to participants. In 2019, parcels of land in Decentraland were swapping hands for around US$500. Today, they are being sold for circa US$10,000, a 20x increase.

Perhaps Twain’s quote should be altered to “Buy tangible land, they’re not making it anymore.”

With the advent of digital assets, has the value proposition of scarce tangible assets been put into question? Our position in CLW implies our stance – there’s enough room in this world (including virtual worlds) for many forms of scarcity.

If you would like further details regarding our activities, we encourage you to follow us on Twitter, where we share more regular bite-sized commentary. Email us at insufficientcapital@gmail.com.